Activity-based costing (ABC) is a method used to allocate overhead and indirect costs based on the activities that drive those costs. In project management, ABC allows for a more accurate understanding of project expenses by identifying and assigning costs to specific activities, rather than using broad allocation methods.

This approach helps project managers make better budgeting, resource allocation and cost control decisions, ultimately improving financial transparency and ensuring projects are completed within budget. Let’s explore ABC costing and the ABC method further.

What Is Activity-Based Costing?

Activity-based costing is a costing method that assigns overhead and indirect costs to specific activities within an organization based on the actual resources they consume. Unlike traditional costing methods that allocate overhead costs based on a single cost driver (such as labor hours or machine hours), ABC focuses on the various activities that contribute to producing goods or services.

The costs associated with each activity (e.g., design, production, distribution or customer service) are calculated and then assigned to products, services or projects based on how much they utilize these activities. This gives a more accurate picture of where costs are incurred in the production process.

The main advantage of activity-based costing is that it allows for more precise cost allocation by recognizing that different products or services may consume resources at different rates. By breaking down costs according to activities, businesses can better understand the true cost of their operations and make more informed decisions about pricing, budgeting and process improvement.

The ABC method is particularly useful for complex organizations or projects with multiple products or services, where traditional costing methods may overlook the detailed costs associated with specific activities. ABC helps businesses identify inefficiencies, eliminate waste and optimize resources for improved financial performance.

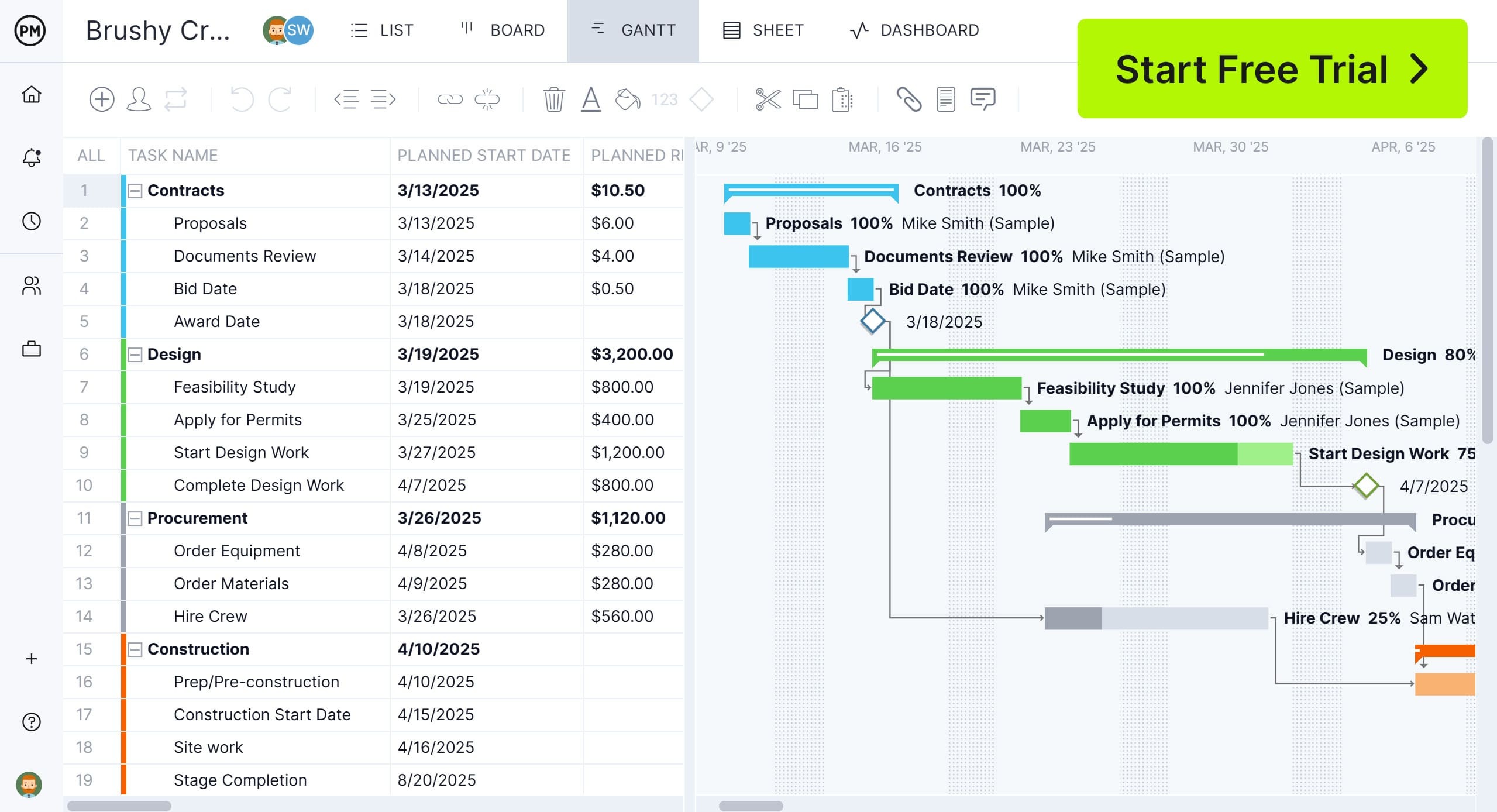

ProjectManager helps with activity-based costing with robust Gantt charts that allow project managers to track, manage and assign costs to specific activities within a project. Use it to create tasks and subtasks for projects, which can then be linked to specific activities that will incur costs. Each task can have resources assigned to it, and the costs for these resources can be tracked directly.

This enables you to assign and allocate costs to individual activities, which is the essence of ABC costing. Plus, our Gantt links dependencies to avoid cost overruns, filters for the critical path and can set a baseline to track costs and more in real time. Get started with ProjectManager today for free.

Activity-Based Costing Steps

The ABC method helps businesses understand the true cost of producing goods or delivering services, which leads to more informed decisions about pricing, budgeting and resource allocation. Here are the key steps in the ABC process.

1. Identify Activities

The first step in activity-based costing is to identify the key activities that consume resources in the production process. These activities could range from design, procurement and production to distribution and customer service. By identifying the activities, you ensure no critical cost-driving actions are overlooked, leading to a clearer view of where resources are used.

2. Group Activities into Cost Pools

Once the activities are identified, they are grouped into cost pools, which are categories that group similar activities. For example, activities like machine maintenance, quality control and assembly might all fall under a production cost pool. Grouping activities into cost pools helps simplify the allocation process and makes it easier to assign costs systematically.

3. Define Cost Drivers

Next, define cost drivers for each activity or cost pool. A cost driver is a factor that directly influences the cost of an activity. For example, the number of machine hours might be the cost driver for machine maintenance, or the number of customer orders might be the cost driver for order processing. Identifying the correct cost drivers is crucial because they determine how costs will be allocated.

4. Calculate Cost Driver Rates

Once the cost drivers are identified, calculate the cost driver rates. This involves determining the cost per unit of the cost driver. For example, if machine maintenance is $100,000 for 10,000 machine hours, the cost driver rate would be $10 per machine hour. These rates help allocate overhead costs based on how much of the cost driver each product, service or project uses.

5. Allocate Costs to Products or Services

Using the cost driver rates, costs are then allocated to specific products or services based on their consumption of the cost drivers. For example, if a product uses 500 machine hours, and the cost driver rate is $10 per hour, the allocated cost for that product would be $5,000. This step ensures that each product or service receives a fair share of the total overhead costs.

6. Take Actions to Minimize Costs and Maximize Profits

The final step is to use the data from the ABC technique to take actions to minimize costs and maximize profits. By understanding which activities are the most expensive and which products or services consume the most resources, businesses can make informed decisions about process improvements, cost-cutting strategies and pricing adjustments. For example, a company might decide to streamline a high-cost activity, eliminate inefficiencies or adjust prices to reflect the true cost of production.

By following these steps, activity-based costing provides businesses with a clearer understanding of their cost structure and helps optimize resource use, leading to better financial performance and strategic decision-making.

Activity-Based Costing Example

That’s all abstract, even with examples for each step. To better understand how the ABC technique works, let’s look at a real-life scenario about a furniture company that manufactures different chairs.

A furniture manufacturing company produces two types of chairs: standard chairs and luxury chairs. The company incurs various overhead costs related to production, such as machine maintenance, material handling and quality inspection. Instead of using traditional costing, the company implements activity-based costing to allocate costs more accurately.

Step 1: Identify Activities and Cost Pools

The company identifies three key activities and groups related costs into cost pools.

- Machine Maintenance: $50,000

- Material Handling: $30,000

- Quality Inspection: $20,000

- Direct Labor: $60,000

- Factory Overhead: $40,000

Step 2: Determine Cost Drivers

The company selects cost drivers for each activity.

- Cost Pool: Machine Maintenance – Cost Driver: Machine hours

- Cost Pool: Material Handling – Cost Driver: Number of material moves

- Cost Pool: Quality Inspection – Cost Driver: Number of inspections

- Cost Pool: Direct Labor – Cost Driver: Direct labor hours

- Cost Pool: Factory Overhead – Cost Driver: Direct labor hours

Step 3: Calculate Activity Rates

Determine the cost per unit of the cost driver, which helps allocate overhead costs to specific activities based on their consumption.

- Machine Maintenance: $50,000 /5,000 machine hours = $10 per machine hour

- Material Handling: $30,000/3,000 material moves = $10 per move

- Quality Inspection: $20,000/2,000 inspections = $10 per inspection

- Direct Labor: $60,000/4,000 labor hours = $15 per labor hour

- Factory Overhead: $40,000/4,000 labor hours = $10 per labor hour

Step 4: Allocate Costs to Products

Assign the calculated activity rates to specific products or services based on their usage of the identified cost drivers.

Standard Chairs (Usage Data)

- Machine Hours: 3,000 × $10 = $30,000

- Material Moves: 1,500 × $10 = $15,000

- Inspections: 1,000 × $10 = $10,000

- Labor Hours: 2,000 × $15 = $30,000

- Overhead (Labor-Based): 2,000 × $10 = $20,000

- Total Cost Allocation for Standard Chairs: $105,000

Luxury Chairs (Usage Data)

- Machine Hours: 2,000 × $10 = $20,000

- Material Moves: 1,500 × $10 = $15,000

- Inspections: 1,000 × $10 = $10,000

- Labor Hours: 2,000 × $15 = $30,000

- Overhead (Labor-Based): 2,000 × $10 = $20,000

- Total Cost Allocation for Luxury Chairs: $95,000

Traditional Costing vs. Activity Based Costing

Traditional costing and activity-based costing are two methods used to allocate overhead costs in an organization, but they differ significantly in approach and accuracy. Traditional costing assigns overhead expenses based on a single cost driver, such as direct labor hours or machine hours.

This method is simpler and easier to implement, making it suitable for businesses with uniform production processes and minimal variability in overhead costs. However, because it applies a broad allocation method, traditional costing can sometimes lead to inaccurate cost distribution, potentially distorting product pricing and profitability.

In contrast, activity-based costing takes a more detailed and accurate approach by assigning costs based on specific activities that consume resources. Instead of relying on a single cost driver, the ABC method identifies multiple cost drivers, such as machine setups, inspections or order processing, to allocate expenses more precisely.

ABC technique is particularly beneficial for companies with complex operations, multiple product lines or high overhead costs, as it provides a clearer understanding of how different activities contribute to total expenses. Although activity-based costing requires more data collection and is more complex to implement, it offers better insights for decision-making, cost control and process improvement.

Ultimately, while traditional costing remains a practical option for simpler businesses, the ABC technique is the preferred choice for organizations looking for precise cost allocation and improved financial decision-making.

Advantages of Activity-Based Costing

Activity-based costing provides a more precise method for allocating overhead costs by linking expenses to specific activities. This approach enhances cost accuracy and supports better financial decision-making.

- Assigns costs based on actual resource consumption, reducing distortions

- Provides precise cost data for pricing, budgeting and profitability analysis

- Helps pinpoint high-cost activities, leading to process improvements

- Enables businesses to eliminate waste and optimize resource allocation

- Reveals true costs of products/services, ensuring better financial planning

- Helps make informed choices about product lines, pricing and efficiency improvements

Disadvantages of Activity-Based Costing

While activity-based costing provides more accurate cost allocation, it also comes with certain challenges. Its complexity and resource-intensive nature can make implementation difficult for some businesses.

- Requires significant time, effort and investment to set up

- Involves detailed tracking of activities and cost drivers, increasing administrative workload

- Requires extensive data gathering, which can be challenging in large or diverse organizations

- May not provide enough added value for companies with simple production processes

- Cost drivers and activities may change over time, requiring continuous monitoring and adjustments

- Staff may resist adoption due to the additional workload and process changes

Related Project Management Templates

There are multiple free templates available to help with activity-based costing. Our site has over 100 free project management templates for Excel and Word that cover all aspects of managing a project across multiple industries. Below are just a few examples that can help manage costs.

Timesheet Template

Download this free timesheet template for Excel to track the hours worked by team members or employees. This weekly summary of start time, lunch, quitting time as well as overtime can be used for time management, but also track labor costs.

Workload Analysis Template

Managing workload helps to balance resource allocation across the project team. This free workload analyst template for Excel helps keep team members from being overallocated or underutilized, which prevents burnout and keeps projects on budget.

Budget Dashboard

A budget dashboard is a visual tool that uses charts and graphs to show important financial metrics, such as planned costs vs. actual costs. Use this free budget dashboard in Excel to monitor costs to stay on budget.

How ProjectManager Helps With Activity-Based Costing

Templates aren’t ideal for managing projects. In terms of costs, they’re always going to be behind. That’s because there are static documents that must be manually updated. Therefore, they’re absolute by the time they’re viewed. Use project management software for more effective cost management. ProjectManager is award-winning project and portfolio management software that has multiple activity planning, schedule and tracking tools to plan, manage and monitor costs in real time.

Manage Resources to Deliver on Schedule and Budget

Resources are anything needed to execute the project tasks. Getting the most out of those resources as efficiently as possible saves time and money. That Gantt chart schedules resources, but then to get an overview of resource allocation, view the color-coded workload page. It shows who is overallocated or underutilized across all projects.

Then balance the team’s workload from that chart to keep everyone working at capacity without worrying about burnout. There’s also a team page that summarizes team activity, either daily or weekly, and can be filtered to view priority, progress and more. Tasks can even be updated without leaving the page.

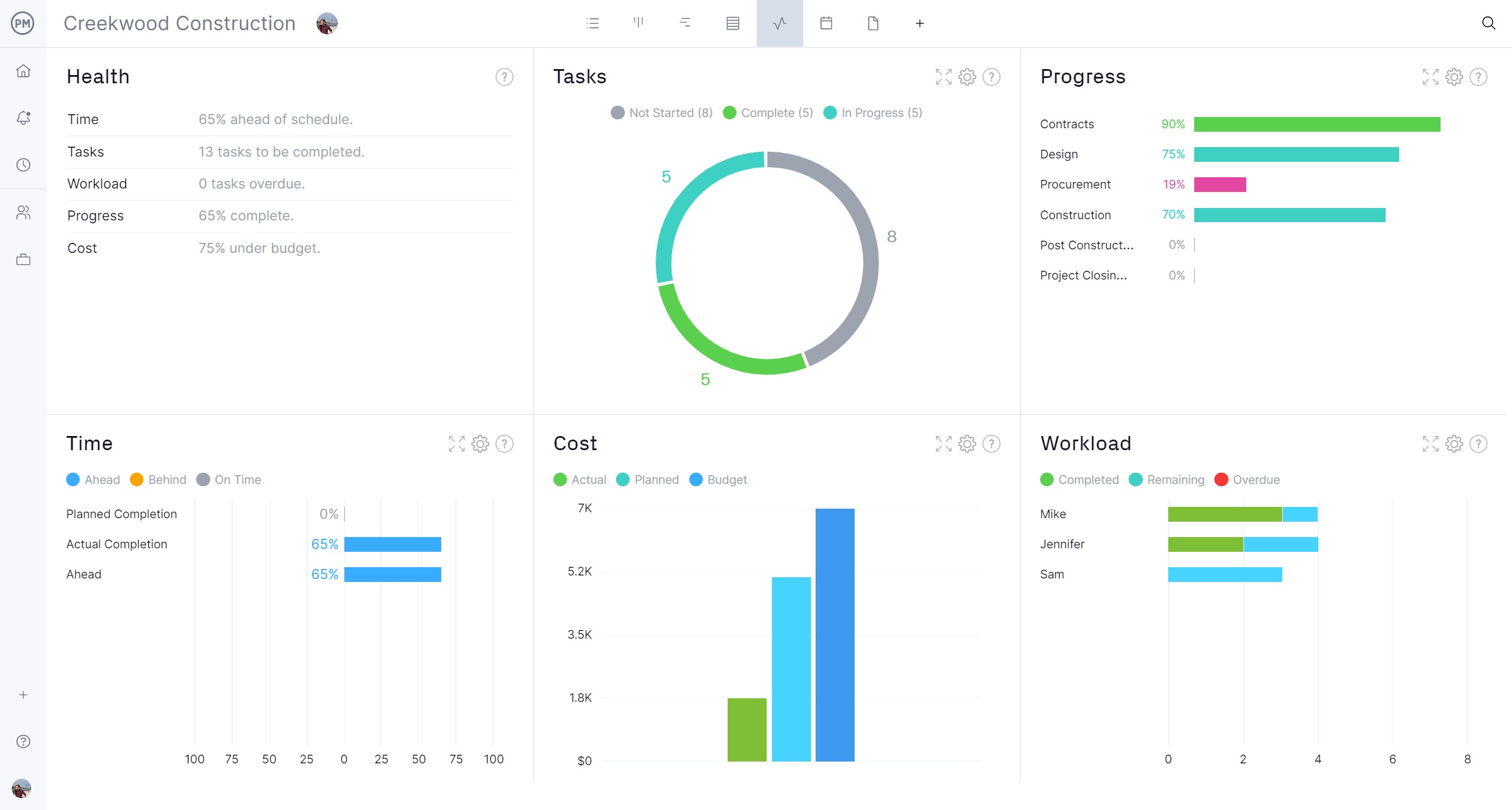

Track Costs With OnlineDashboards and Reports

Resources are only one metric to measure. Get a high-level overview of key performance indicators (KPIs) by toggling over to the real-time project or portfolio management dashboard. It displays time, cost, workload and more in easy-to-read graphs and charts.

Customizable reports go deeper and can be generated with a keystroke. Create project or portfolio status reports or reports on variance, timesheets, workload and more. Filter for specific data points or more general info to share with stakeholders. Even secure timesheets can help stay on budget by tracking labor costs.

Related Content

Activity based costing is only one way to control costs in project management. To learn more, check out the links below. They lead to some of our more recent pieces on job costing, cost control techniques and more.

- What Is Job Costing? When to Use a Costing Sheet

- 15 Best Cost Control Techniques

- Cost Control in Project and Business Management

- Cost of Production: Types of Production Costs

- What Is a Cost Baseline in Project Management?

ProjectManager is online project and portfolio management software that connects teams whether they’re in the office or out in the field. They can share files, comment at the task level and stay updated with email and in-app notifications. Join teams at Avis, Nestle and Siemens who use our software to deliver successful projects. Get started with ProjectManager today for free.